12 Essential Criteria for Emerging VC Managers in 2026

LPs have become more selective and more structured than ever. This guide breaks down 12 criteria that help emerging VC managers earn trust and win commitments.

If you are an emerging VC manager in 2026, you are entering a market that is already data-driven. Private markets do look attractive on long-term performance charts. However, cash is not returning quickly enough, so LPs have tightened their standards on who they invest in and how they size commitments.

Long-term benchmarks, such as the Cambridge Associates indices, show that diversified private equity has delivered low double-digit pooled net returns over multi-decade horizons. At the same time, top-tier managers and some vintages can reach the mid-to-high teens. Distributions have lagged since 2022, with payouts as a share of NAV near historic lows even as secondary volumes hit records.

LPs are not walking away, but they are far more selective, especially with first and second-time managers who still have to prove they can turn paper gains into real DPI.

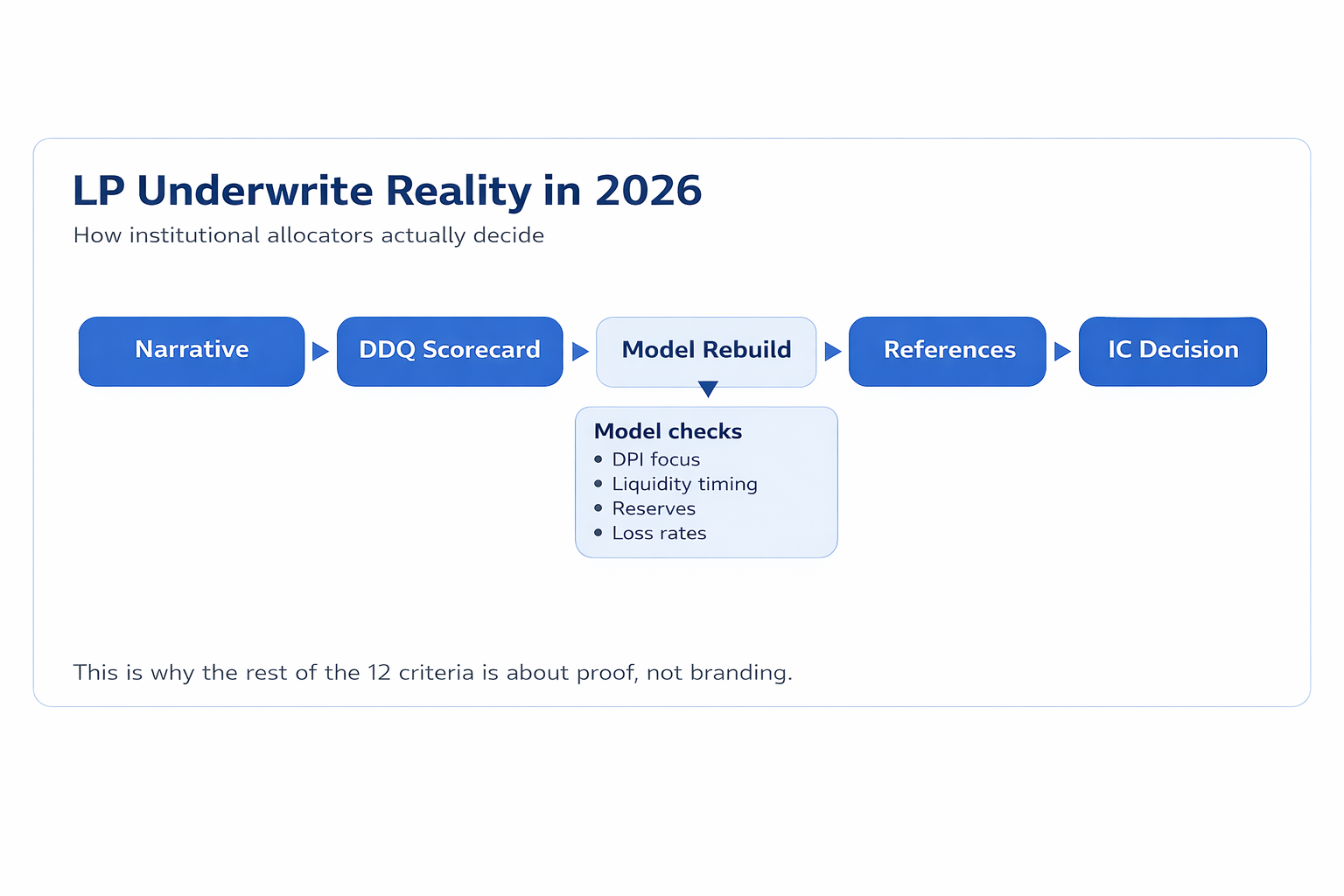

In this case, LPs do not fund any name or brand. They fund proof. Many institutional allocators now rely on structured ILPA-style questionnaires and internal scorecards when they underwrite emerging managers.

Check out the ILPA questionnaire: https://ilpa.org/resources-tools/resource-library/due-diligence-questionnaire/

These 12 points will guide you on how to design your firm, pitch and data room to match how they think.

1. Team and roles

LPs start with people. They want a cohesive group covering sourcing, underwriting, operating and portfolio management. They also want evidence that you have worked together in real situations, not only on a slide.

Get a one-page “Firm and Team” note ready explaining role split, decision dynamics and a short list of founder and colleague references LPs can call.

2. Proxy track record

Without a prior fund with audited numbers, LPs expect a proxy track record. That comes from angel cheques, scout investments and deals you led at earlier platforms, with clear attribution for who sourced, led and supported each.

Maintain this in a simple spreadsheet and turn it into a short deck with five to ten positions and outcomes.

3. Investment thesis

Generic “early stage, sector agnostic” language no longer works. LPs want a straight strategy and a clear link between that strategy and your background. They also want proof that you understand the market using real data.

Draft a thesis memo that defines your segment, explains why incumbents are missing it and lists a few testable insights you expect to hold over a decade.

4. Deal flow and founder pull

Venture is an access game. LPs ask whether you are in the right conversations and whether strong founders pick you when rounds are competitive.

Track a simple sourcing dashboard with monthly qualified opportunities, inbound share, referral channels and win rates. Use that chart in LP meetings to make your network advantage visible.

5. Portfolio construction and fund math

Here, LPs move from story to spreadsheet. They rebuild your fund model from scratch to test whether your target DPI and net multiple are realistic.

Build a transparent model that fixes fund size, core positions, target ownership, reserves and loss rates. Then show the base and upside DPI over ten to twelve years for your market.

6. Value creation for founders

Every deck says “hands on”, so LPs ignore the phrase unless you show concrete value creation.

Assemble a short founder impact appendix with three to five cases where you helped close key hires, bring in customers or arrange bridge rounds. Add simple metrics so LPs can see how your involvement moved revenue or runway.

7. Liquidity and DPI plan

Exit markets slowed sharply after the 2021 peak. Distributions to NAV have dropped to levels not seen since the GFC. As a result, liquidity design now sits near the top of LP question lists. Many LPs and GPs are using secondaries and continuation funds to manage exposure.

Include a “Liquidity and DPI” slide that outlines the likely mix of trade sales, IPOs, secondaries and continuation funds for your portfolio. Give broad bands for the first and peak distributions.

8. Economics and alignment with LPs

LPs examine your economics to see whether you are truly aligned with them through good and bad cycles.

Share full terms early. Include fee path, carry, expense policy and GP commitment in absolute dollars and as a percentage of the fund. Be explicit about how partners are funding those commitments.

9. Investment process and governance

Institutional LPs expect a recognisable investment committee process and basic governance, even in Fund I.

Prepare a one-page IC and governance summary, plus a couple of redacted memos and post mortems. Show who has approval authority, how often you meet, how you handle conflicts and how you learn from mistakes.

10. Operational infrastructure

Even for a first-time vehicle, a do-it-yourself operational stack is a warning sign.

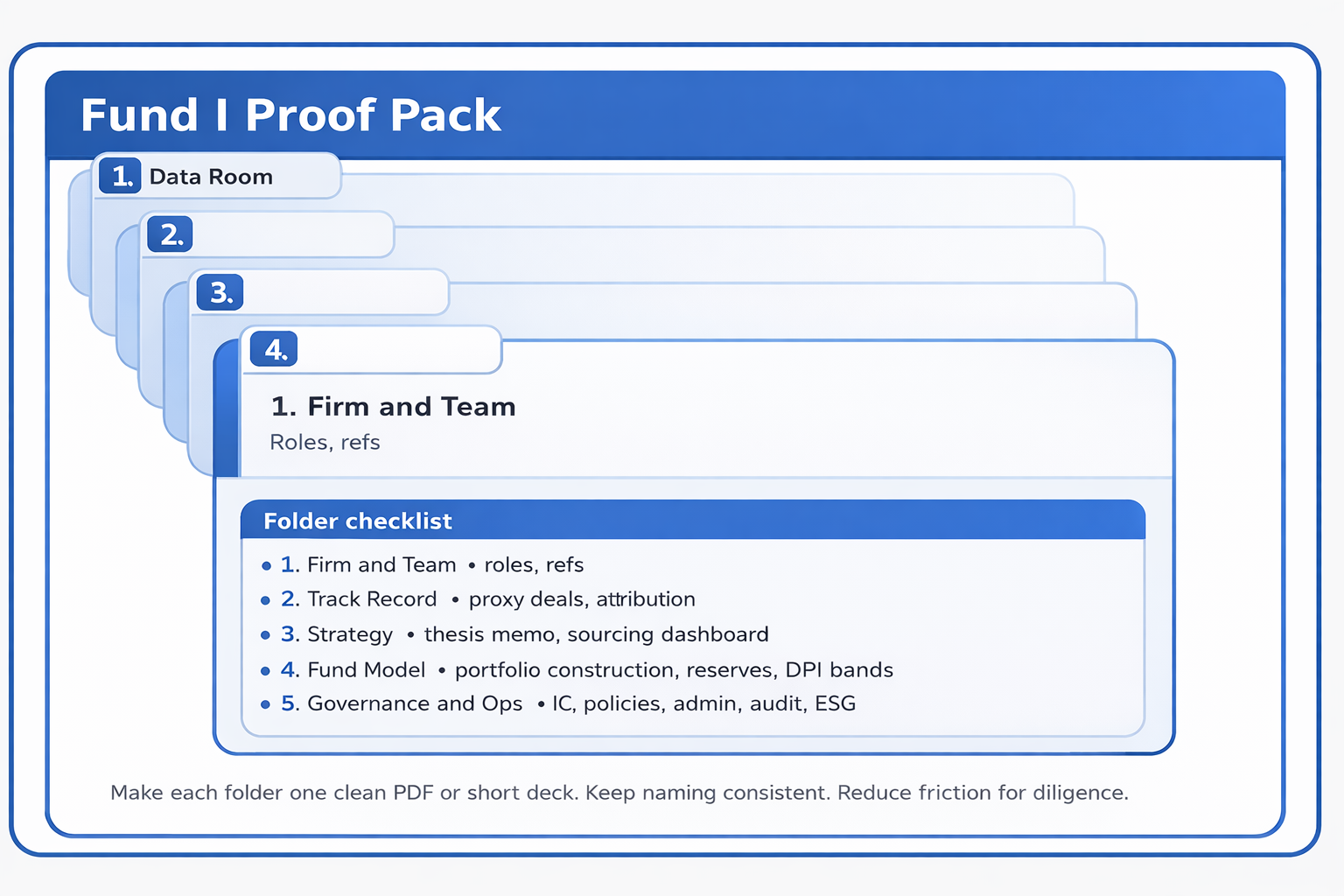

Appoint an independent fund administrator and experienced legal and audit firms. Adopt straightforward policies on valuation, cybersecurity and ESG. Structure your data room along familiar DDQ headings.

11. Fundraising traction and momentum

LPs also read your cap table when they decide whether to join it. They want to know who has already done the work.

Maintain a simple fundraising snapshot with target, soft cap, hard cap and percentages signed, in docs and in late-stage discussions. Add a short list of anchor and reference LPs who have already gone deep on diligence.

12. Mission, ESG and diversity

Mission, ESG and diversity now sit in the core of institutional LP diligence rather than on a feel-good slide. ILPA templates and in-house questionnaires at many organisations hard-code this into the process.

Track basic diversity metrics for your team and founders. Describe your sourcing approach across networks. Document a few examples where ESG or mission considerations changed a yes or no decision.

No doubt, LPs in 2026 are operating under real liquidity constraints and scrutiny is intense. They still want new managers who can turn paper value into real, repeatable DPI. Use these criteria as a design brief and you move from sounding like a hopeful GP to sounding like a partner they can trust for the next decade.

_________________________

About Taghash

Taghash provides an end-to-end platform for venture funds, private equity, fund of funds, and other alternative investment funds. Over the last seven years, we have served as the tech arm for top VCs, helping them manage operations across deal flow, portfolio, fund, and LP management.

Trusted by leading fund managers like Blume Ventures, Kalaari Capital, and A91 Partners, we enable our clients to achieve greater success. Click here to book a demo.