All About Continuation Vehicles

This blog breaks down how continuation vehicles work. It explains who benefits, what can go wrong and how India’s growing exit market is enabling smarter, long-term structures for investors and founders.

Most venture capital (VC) funds have a base life of around 10 years, often with extension options.

As they near the end of that period, funds are under pressure to exit or distribute holdings and return money to investors, even if some of their investments are just hitting their stride.

But what if a fund could keep supporting such companies a little longer, without breaking its promise to investors?

That’s where a structure called a Continuation Vehicle (CV) comes in.

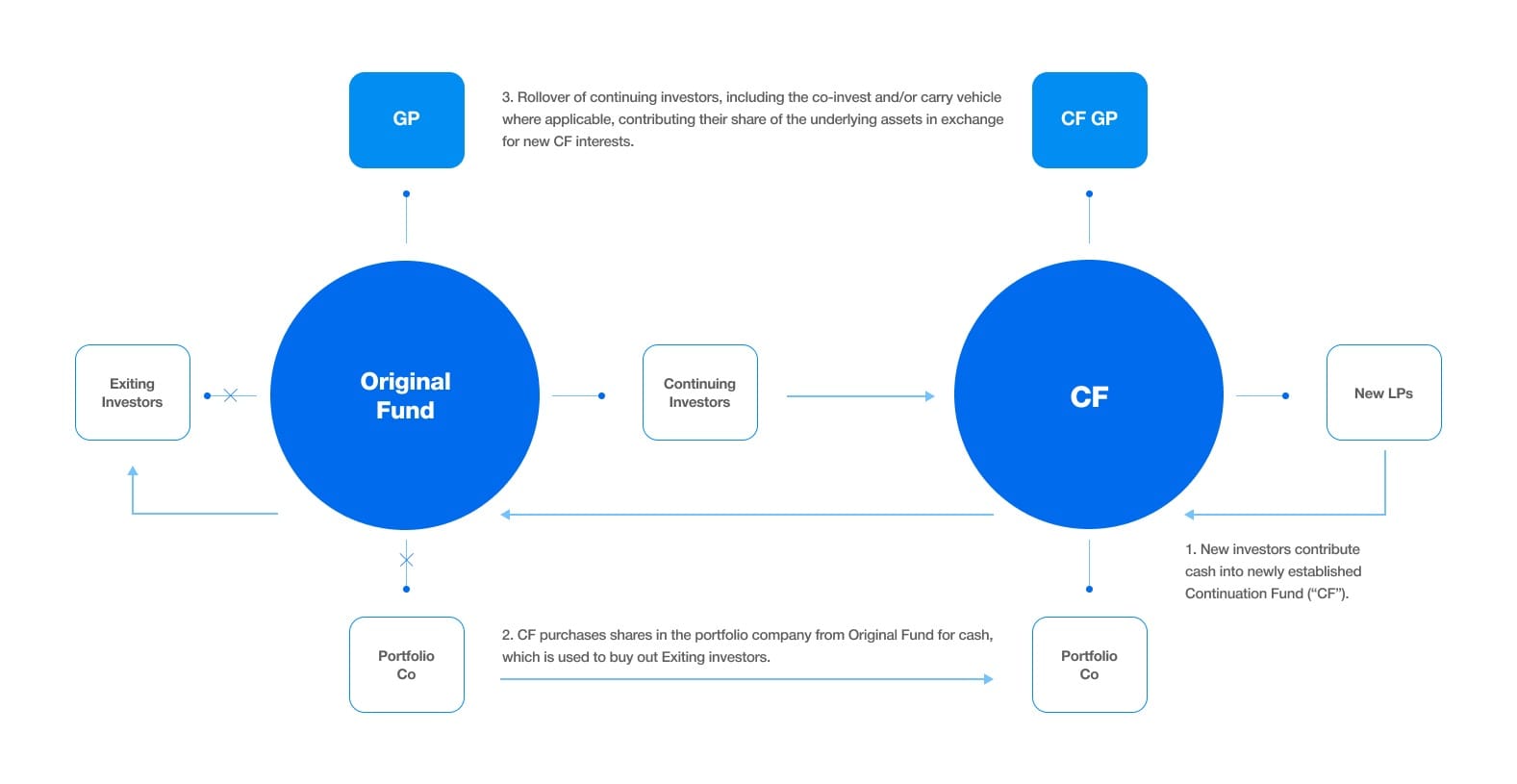

What exactly is a Continuation Vehicle?

Think of it as a new fund created by the same fund manager, designed to extend the holding period for some of its investments.

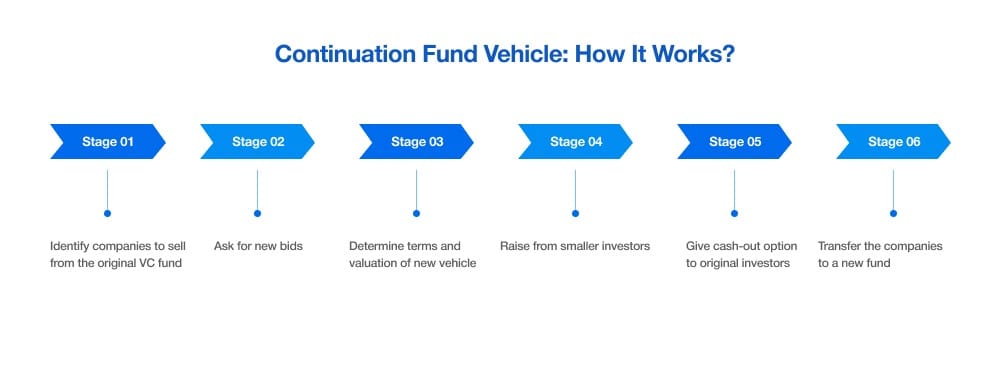

Here’s how it works in simple steps:

1. Selection: The fund manager picks one or more strong, high-potential companies that still have a lot of growth ahead.

2. Fair Pricing: As they near the end of that period, funds are under pressure to exit or distribute holdings and return money to investors, even if some of their investments are just hitting their stride.

3. Creation: A new vehicle (the CV) is set up to buy those shares from the old fund.

4. Investor Choice: The original investors (called LPs) get two clear options:

- Option 1: Cash Out - Take their returns now and get immediate liquidity.

- Option 2: Roll Over - Move their stake into the new vehicle and stay invested for the next big win.

5. Continuation: The fund manager keeps supporting the company until it’s ready for a major milestone like another investing round or a blockbuster IPO, within the CV’s own multi-year holding period.

For example, imagine a fund invested in Startup A in 2018 and the fund is nearing the end of its term in 2026. Startup A is doing well but needs two more years to unlock a massive IPO valuation. The CV buys the shares, gives existing investors cash or the choice to reinvest and the manager holds Startup A until its successful IPO in 2028.

In short, it’s like saying, “Let’s not rush the finish line. Let’s give this champion runner more time to break the record.”

Why this matters right now

India’s venture capital ecosystem has grown massively from about $400 million in 2012-13 to nearly $13.7 billion in 2024.

That means there are now hundreds of mature, late-stage startups that just need a bit more time to realise their full value.

The problem

VC funds run on fixed timelines. Traditional exits like IPOs or acquisitions can take years. Without a flexible option, funds might be forced to sell great companies too early - often at a discount.

The solution

Continuation Vehicles can help avoid these “fire sales.” They let fund managers stay focused on long-term value instead of being pressured by an arbitrary 10-year clock.

Global and National perspective

Globally, continuation vehicles have become a mainstream tool in the secondary market, especially in buyout funds. In 2024, the total global secondary-market volume reached about $162 billion and GP-led deals made up the mid-40s of that total. While buyout funds still dominate, continuation vehicles are steadily expanding into growth-stage and venture portfolios as well.

India now accounts for around 21% of continuation-vehicle activity across emerging markets, by number of completed CVs from 2020 to H1 2025. A highlight example came in 2025, when Multiples Alternate Asset Management closed India’s largest multi-asset continuation vehicle worth $430 million. This confirms how mainstream the structure is becoming.

Who actually benefits?

Investors (LPs): They can choose between taking cash now or staying in for potentially bigger gains later.

Founders: They get patient capital and less pressure to exit early, allowing them to build stronger and more sustainable companies.

Fund Managers (GPs): They can hold on to their best assets and focus on long-term growth instead of rushing toward closure.

It’s a win-win-win as long as the process stays fair, transparent and well executed.

What could go wrong (and how to avoid it)

Like any financial structure, continuation vehicles require discipline and checks:

- Like any financial structure, continuation vehicles require discipline and checks: Fair pricing is critical so that the negotiated price is supported by independent valuation or a fairness opinion, keeping everyone on the same page.

- Only high-quality companies should be moved into these vehicles. Weaker or tail-end assets often face 30-40% valuation discounts, which can create friction, while higher-quality portfolios often trade much closer to NAV.

- Documentation and communication must remain clean and transparent.

If handled properly, continuation vehicles strengthen the ecosystem; otherwise, they can create confusion and distrust as well.

The bigger picture

Continuation vehicles aren’t just financial tools; they’re a sign of maturity. They show that India’s venture capital system is evolving from building startups to building smarter exits.

Discipline, choice and timing are the factors that separate smart investing from lucky investing.

India’s exit market is maturing too. Private-equity and venture exits touched $33 billion in 2024, a 16% year-on-year increase, proving that the ecosystem is becoming more sophisticated and ready for advanced fund structures like CVs.

_________________________

About Taghash

Taghash provides an end-to-end platform for venture funds, private equity, fund of funds and other alternative investment funds. Over the last seven years, we have served as the tech arm for top VCs, helping them manage operations across deal flow, portfolio, fund, and LP management. Trusted by leading fund managers like Blume Ventures, Kalaari Capital and A91 Partners, we enable our clients to achieve greater success. Click here to book a demo.