Building a Winning Investment Portfolio

Portfolio construction is how you increase your odds of owning the outliers that drive venture returns. This blog breaks down strike zone, bet count, cheque sizing with follow-on reserves and liquidity planning so your fund is built for a power law outcome distribution.

If you have been to enough LP or investment committee meetings, you may have noticed a pattern. Nobody really believes every company will work. What they care about is whether your portfolio gives you a fair shot at the one or two outliers that pay for everything else.

That is the power law at work, where a small number of companies generate a large share of returns and consistently appear in venture data and benchmarks.

Designing an investment portfolio is, indeed, about respecting that power law while keeping the language clean and direct. You do not need complex models, but you do need a clear view of where you invest, how many bets you make, how much you own when something works and how you turn paper gains into cash over time.

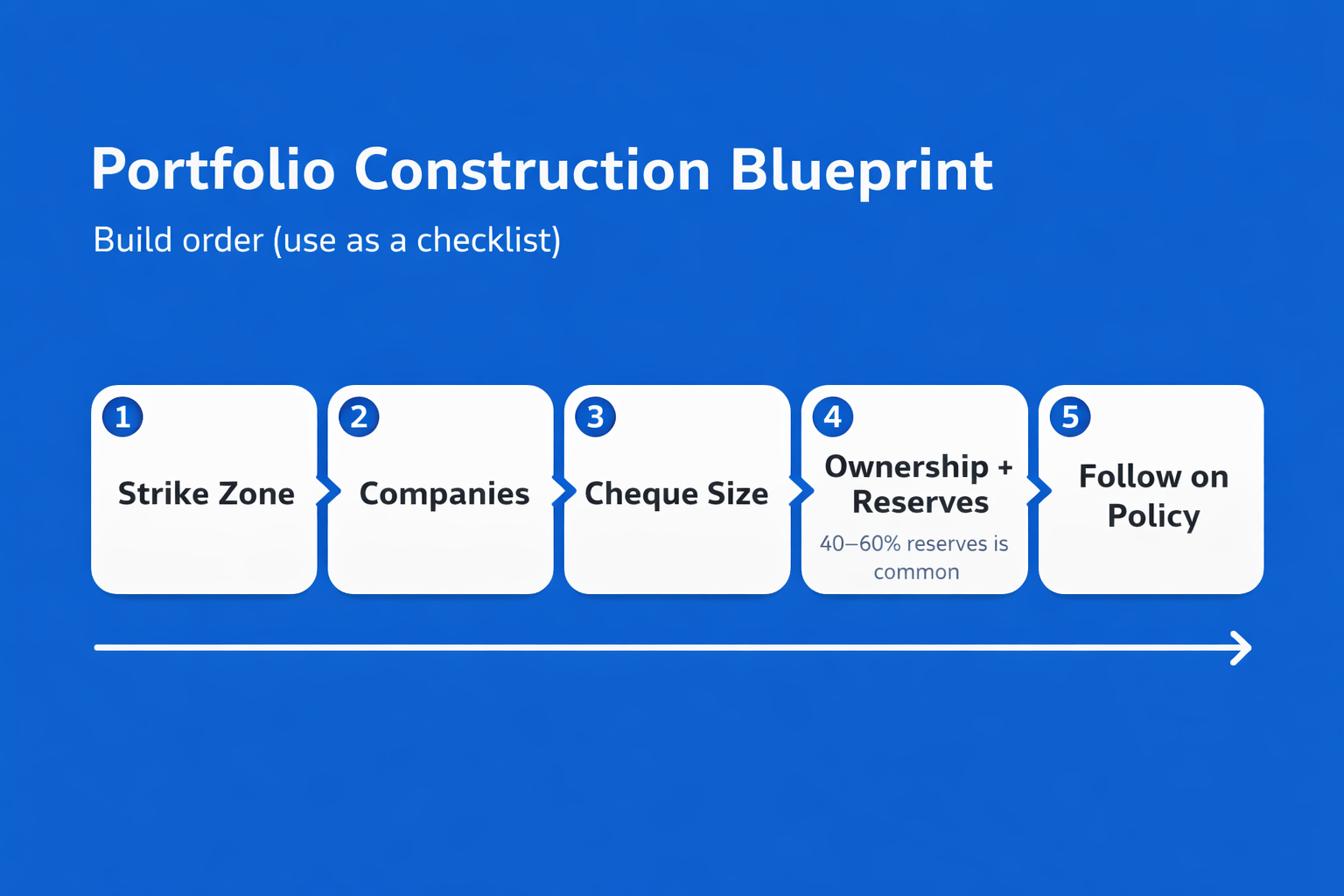

1. Start with your strike zone: where you actually play

Before spreadsheets and return targets, good investors start with something much more human: what are we actually good at?

In venture, people call this your strike zone - the specific mix of sector, stage and geography where you want most of your deals to settle. A fund that knows it backs seed-stage B2B SaaS in India and South-East Asia will filter opportunities very differently from one that chases late-stage consumer deals in the US.

Why does this matter for portfolio design? Because the power law doesn’t reward random activity, it rewards you for recognising outliers earlier and more often than the rest of the market. Focused strike zones make that possible.

Global data shows that venture is still highly concentrated in a few hubs like the US, China and an expanding group of ecosystems like India and Europe, but within that, top funds specialise tightly by sector and stage. A clear strike zone helps you get into the right rooms, see repeat patterns in similar companies and avoid stretching into areas where you have no real edge.

2. Choose a realistic number of companies and cheque sizes

Once you know your strike zone, the next building block is surprisingly basic: how many companies do you want to back and with what initial cheque size?

Most early-stage funds that LPs take seriously fall in a band of roughly 20 to 30 portfolio companies; that range comes up repeatedly in emerging-manager guides and fund-of-funds commentary.

So, if you only back five or six companies, even one or two failures can crush the fund, and you may simply never intersect with a true outlier. If you back 60 or 70 with very tiny cheques, you spread yourself thin and don’t own enough of any winner to move the needle.

A 50 million dollar fund, for example, might decide on 22–25 core positions with average initial cheques of 1.5–2 million dollars each. That gives enough “shots on goal” in the chosen strike zone while still leaving room in the fund for follow-on capital and fees.

3. Think in ownership and reserves, not just “number of bets”

Where portfolio construction becomes more “VC native” is when you stop thinking only in names and cheques and start thinking in ownership and reserves.

Ownership is your percentage stake in each company. Reserves are the portion of your fund kept back for follow-on rounds in companies that start to work. Because venture returns are so skewed, owning 1-2% of a unicorn versus 10-15% of the same company can be the difference between a nice story and a fund-returning outcome.

Industry aimed at GPs are remarkably aligned on one point: serious funds keep a large share of capital for follow-ons, often 40 to 60% of the fund, so they can defend their pro rata or even lean in when winners emerge.

A common structure for an early-stage vehicle is something like 60-65% of capital for initial cheques and 35-40% reserved for follow-ons in the top 20-30% of companies. In practice, that means when a portfolio company raises a strong Series A or B, you can participate meaningfully instead of watching your ownership dilute away.

4. Build simple fund math around the power law

With strike zone, portfolio count, cheque size, ownership and reserves roughly defined, you can finally ask: does this fund design have any chance of hitting LP expectations?

Large LPs often use data from firms like Cambridge Associates to benchmark venture performance. Their long-run numbers show that while the asset class as a whole can outperform public markets over time, the median fund isn’t spectacular; real outperformance lives in the top quartile.

Because of that, many LPs quietly hope for something like 3× net from a new venture fund over its life. Once you factor in the common “2 and 20” fee and carry structure described in most venture primers, a manager may need to target 4-5× gross TVPI at the portfolio level to land near 3× net.

The way to check this is not with complex Monte Carlo simulations but with a brutally simple table: list, say, 24 hypothetical investments; assume a realistic mix of write-offs, 1-2× outcomes, a few 3-5× and one or two potential 10×+ outliers; apply your target ownership; and see if the total adds up near your gross return target. If it doesn’t, the design is wrong; you either don’t have enough potential outliers or your ownership in winners is too small.

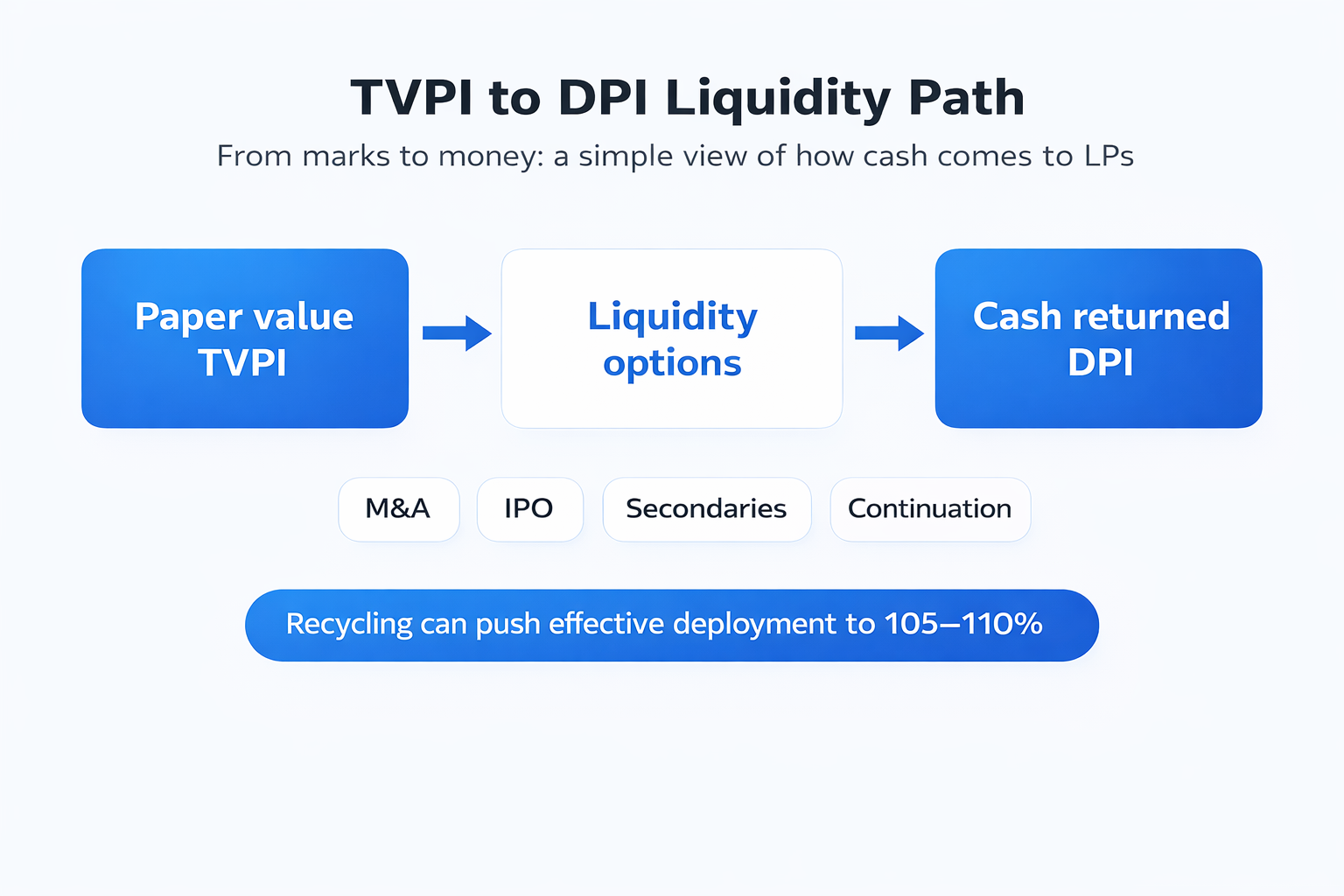

5. Plan ahead for liquidity: from TVPI to DPI

On paper, a portfolio can look fantastic. LPs focus heavily on DPI, i.e, how much cash has actually been distributed back relative to what they put in and not just TVPI (total value, including unrealised gains). After the 2021 peak, IPO windows narrowed and M&A slowed, so managers increasingly used secondary markets and GP-led continuation vehicles to turn marks into money. Global secondary volume in private markets reached roughly $160 billion in 2024, a record level, as reported by major secondary advisors and banks.

A thoughtful liquidity plan recognises this shift. Instead of waiting only for an IPO, you might decide that once a position crosses a certain value and is relatively mature, you will explore selling a slice in a secondary transaction or into a continuation fund while keeping some upside.

At the same time, many LP agreements now allow recycling means reinvesting early distributions or fee offsets into new deals during the investment period. Used carefully, recycling can push effective deployment above 100% of committed capital, often to 105–110%, amplifying the impact of your winners without raising a larger fund.

6. Avoid the classic traps and keep the design honest

When LPs talk about why certain emerging managers fail, the reasons are usually simple and structural rather than exotic, such as:

- Spray and pray: writing many tiny cheques into dozens of companies with no clear strike zone, reserve policy or ownership target.

- No reserve discipline: spending almost all the fund on first cheques, then being unable to follow on in obvious winners, which hurts both the economics and the signal to future investors.

- Incoherent fund math: saying “we are concentrated and high conviction” but quietly planning for 50+ names, or promising multi-stage exposure with a fund too small to support that.

The antidote is to treat portfolio construction like a product spec you actually follow:

- A clear strike zone

- A realistic portfolio size

- Sensible cheque sizing

- Explicit ownership targets

- A written reserve policy

- A one-page fund model that you revisit as the portfolio builds

None of that requires advanced finance skills. It does require accepting how venture really works in a power-law world and designing around it, rather than fighting it.

If you can explain this in simple language: who you back, how many companies, what stake you want, how you support winners and how you expect to return capital, you’ve already done the hard part.

In 2026, that kind of clarity is exactly what LPs and co-investors are looking for when they decide which managers they trust to plant and grow the next generation of outlier companies.

About Taghash

Taghash provides an end-to-end platform for venture funds, private equity, fund of funds, and other alternative investment funds. Over the last seven years, we have served as the tech arm for top VCs, helping them manage operations across deal flow, portfolio, fund, and LP management.

Trusted by leading fund managers like Blume Ventures, Kalaari Capital, and A91 Partners, we enable our clients to achieve greater success. Click here to book a demo.