How cash flows between LPs and GPs: European vs US Waterfall in Private Equity

European vs US waterfall decides when carry is paid and how profits are shared. This blog breaks down both models, explains clawbacks and escrows and shows why hybrids are now common.

When a private equity or VC fund starts returning money, the distribution waterfall decides who gets paid first and how profits are shared between LPs (limited partners) and GPs (general partners).

Most institutional funds use the same basic building blocks:

- LPs get back their contributed capital

- LPs earn a preferred return or hurdle, typically around 7 to 8% per year

- The GP moves through a catch-up slice

- Remaining profits are split, most often 80% to LPs and 20% to the GP as carried interest

The real difference is where you apply this logic and when the carry starts flowing to the GP.

The core difference in one idea

At a high level, you can think of it like this.

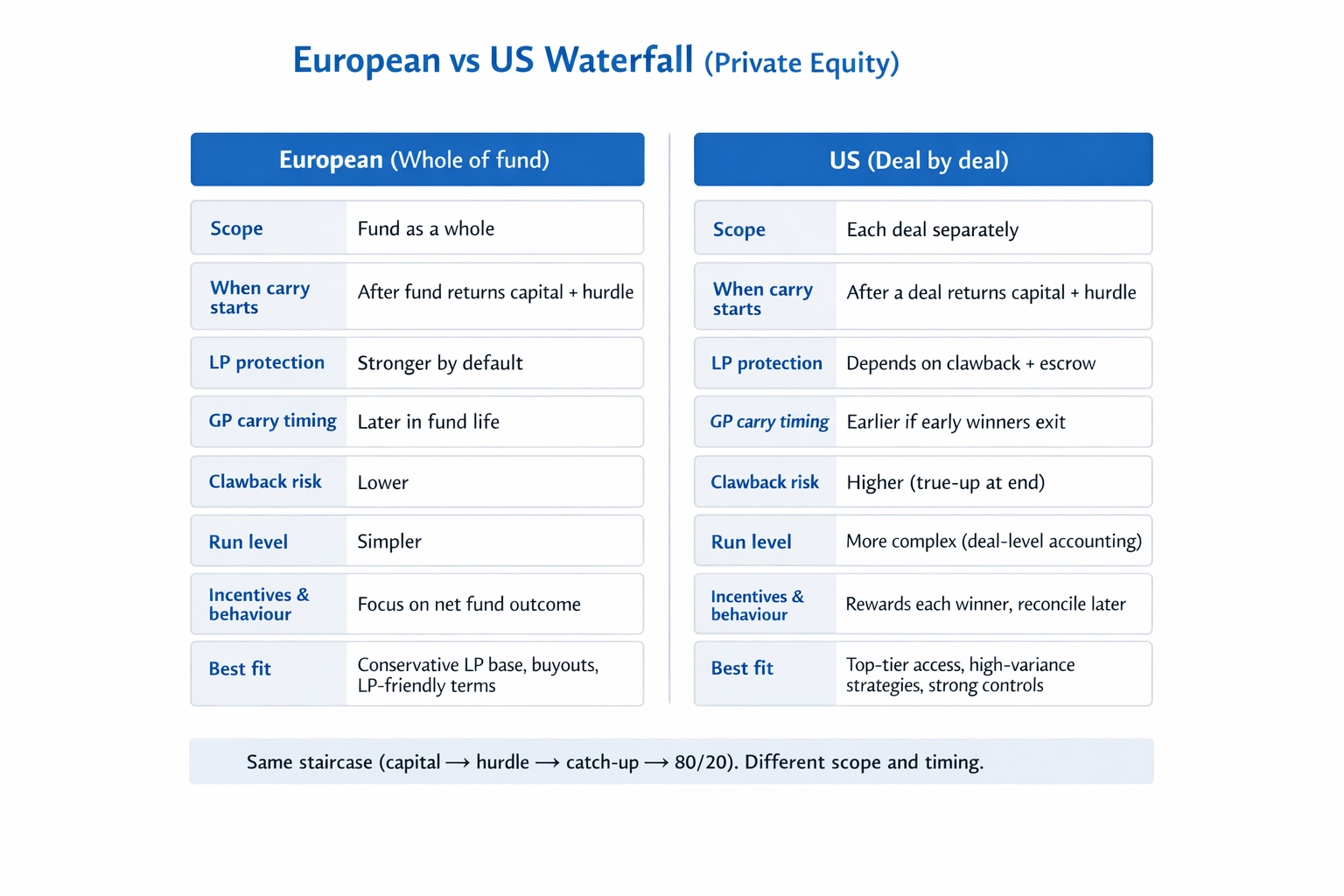

European: fund as a whole waterfall

Carry is calculated after the fund's overall return has returned all contributed capital and cleared the hurdle.

US: deal by deal waterfall

Carry is calculated for each deal once that deal has returned its own capital and hurdle, even if the rest of the fund is still in flux.

It is the same staircase, but applied at different scopes and timings. That is what drives the pros and cons.

European waterfall: “Show me the whole fund first”

In a European-style waterfall, you treat the fund as one big pool. You:

- Add up everything LPs have invested over time.

- Apply the preferred return on that total contributed capital.

- Distribute cash back to LPs until that capital plus hurdle has been fully paid.

Until LPs have received that full amount, no carry is paid. Only once the fund, in aggregate, has cleared this bar does the GP move into catch-up and then the 80 to 20 profit split.

In practice, this means:

- Gains and losses across the portfolio are netted before carry is calculated

- A big early win can be offset by later weak or loss-making exits

- GP upside is linked to net fund performance, not a handful of individual hits

From an LP point of view, European waterfalls feel naturally protective. It is hard for a GP to earn a large carry if the fund ultimately delivers poor overall returns. You see fewer clawback situations and less need to chase GPs for refunds, because carry tends to be calculated later when the portfolio picture is clearer.

The trade-off is timing. Cash returns to LPs as deals exit, but carry for the GP is usually pushed into the back half of the fund’s life. That can affect behaviour and firm design:

- Partners may rely on management fees for longer

- Some teams become more conservative, knowing that they need the whole book to work before they see meaningful carry

You can think of a European waterfall as “We settle the final score for the fund, then we share upside.”

US waterfall: “Pay me on each winner, reconcile later”

In a US or deal-by-deal waterfall, you zoom in on each realised investment.

For every exit, you ask a narrower question. Did this specific deal return:

- Its own contributed capital and

- The hurdle to that capital

If yes, the GP can carry on that deal’s profits. This can happen even while other deals in the fund are still unrealised or later lose money.

This changes how the fund feels for both sides:

- Successful early exits can generate carry in the early years of the fund

- GP economics are tied more directly to individual deals

- If later deals underperform, the GP may have received more carry during the life of the fund than is justified by the final net performance

To correct for that, US-style structures rely on two tools.

- Clawback

A contractual mechanism at the end of the fund that requires the GP to return excess carry so that LPs end up with the agreed share of total profits.

- Escrows or holdbacks

A portion of carry is held back in a separate account until late in the fund's life. This acts as a buffer if clawback is needed.

For GPs, the upside is clear. Earlier carry helps fund partner compensation, retain senior investors and build the platform without waiting a decade. For LPs, deal-by-deal waterfalls can be acceptable with top-tier managers or in higher dispersion strategies, but they require strong clawback mechanics, escrow design and back-office discipline.

In spirit, a US waterfall says, “Reward each winning deal as it happens and we will stay true up at the end.”

LP perspective: how the trade-off looks

From an LP investment committee chair, the choice is mostly about timing and protection.

European waterfall, LP view

You see:

- Strong alignment with net fund performance, since carry appears only when the whole fund has clearly worked

- Lower clawback complexity and less need to chase GPs for refunds later

- A simple story for your own board and regulator: carry only after capital plus hurdle is returned at the fund level

The cost is that GPs are paid later, which can:

- Make some platforms more dependent on management fees

- Reduce appetite for very aggressive, high volatility strategies unless terms are improved elsewhere

US waterfall, LP view

Here you are accepting:

- Earlier carry for GPs on early winners

- Greater reliance on clawback and escrows to protect you if later deals disappoint

- More moving parts to monitor, including deal-level accounting, interim carry and final true-ups

That trade-off can be acceptable when:

- You really want access to a top decile GP

- The strategy is high variance, such as some venture and growth funds, where outlier exits are expected

- You have the internal capability to monitor the mechanics closely

Many conservative institutions, therefore, start negotiations from a default of “European style or a very LP-friendly hybrid, unless the GP is genuinely elite and the strategy demands something different.”

GP perspective: what it does to the firm

For GPs, the waterfall structure is part economics and part culture.

Under a European-style waterfall, carry is back-ended. The firm leans more heavily on management fees and GP commitments to fund the team and platform until the fund matures. This can work well for established, multi-fund houses. It sends an LP-friendly signal: the team is paid on carry only when the whole fund succeeds. It also keeps calculations simpler: one fund level pool to track rather than dozens of separate deal level waterfalls.

The downside is partner patience. Junior and mid-level investment professionals may feel that meaningful upside is far away. Retention can become harder unless you offer other equity, co-invest or bonus schemes.

Under a US-style waterfall, economics are more immediate. A few strong exits early in Fund I or Fund II can transform the firm’s balance sheet. That makes it easier to:

- Attract and retain senior talent

- Invest in sourcing, portfolio support and new geographies

- Build a real franchise quickly

But the firm then lives with:

- Ongoing clawback risk if the overall fund ends below expectations

- More complex finance, tax and legal work

- Potential pushback from some institutional LPs, especially if you are a first-time or relatively unproven manager

So the real question for the GP is: “Given our strategy, track record and target LP base, which pattern supports a sustainable firm without scaring off the investors we want?”

Why hybrids are common now

Because a pure European waterfall tends to favour LPs on timing and a pure US waterfall tends to favour GPs on timing, many modern funds land on hybrid waterfalls.

Typical hybrid features include:

- A requirement that the fund returns 100% of drawn capital and, in some cases, all or part of the hurdle at the fund level before any carry is paid

- Once that threshold is crossed, subsequent realisations can pay carry on a more deal-by-deal basis

- A portion of the carry is kept in escrow until near the end of the fund to cushion any clawback

This gives LPs a fund-level safety buffer and gives GPs earlier upside once the fund is significantly de-risked. The exact thresholds, percentages and escrow rules vary, but the logic is the same. Risk and timing are shared in a way both sides can live with.

Regulation nudges these choices too. European regimes such as AIFMD tend to push for more transparency and more fund-level thinking when it comes to performance and remuneration. US practice is more flexible, as long as terms are clearly disclosed and all parties understand the economics. In markets like India, AIFs often lean closer to European-style or conservative hybrid structures as a starting point.

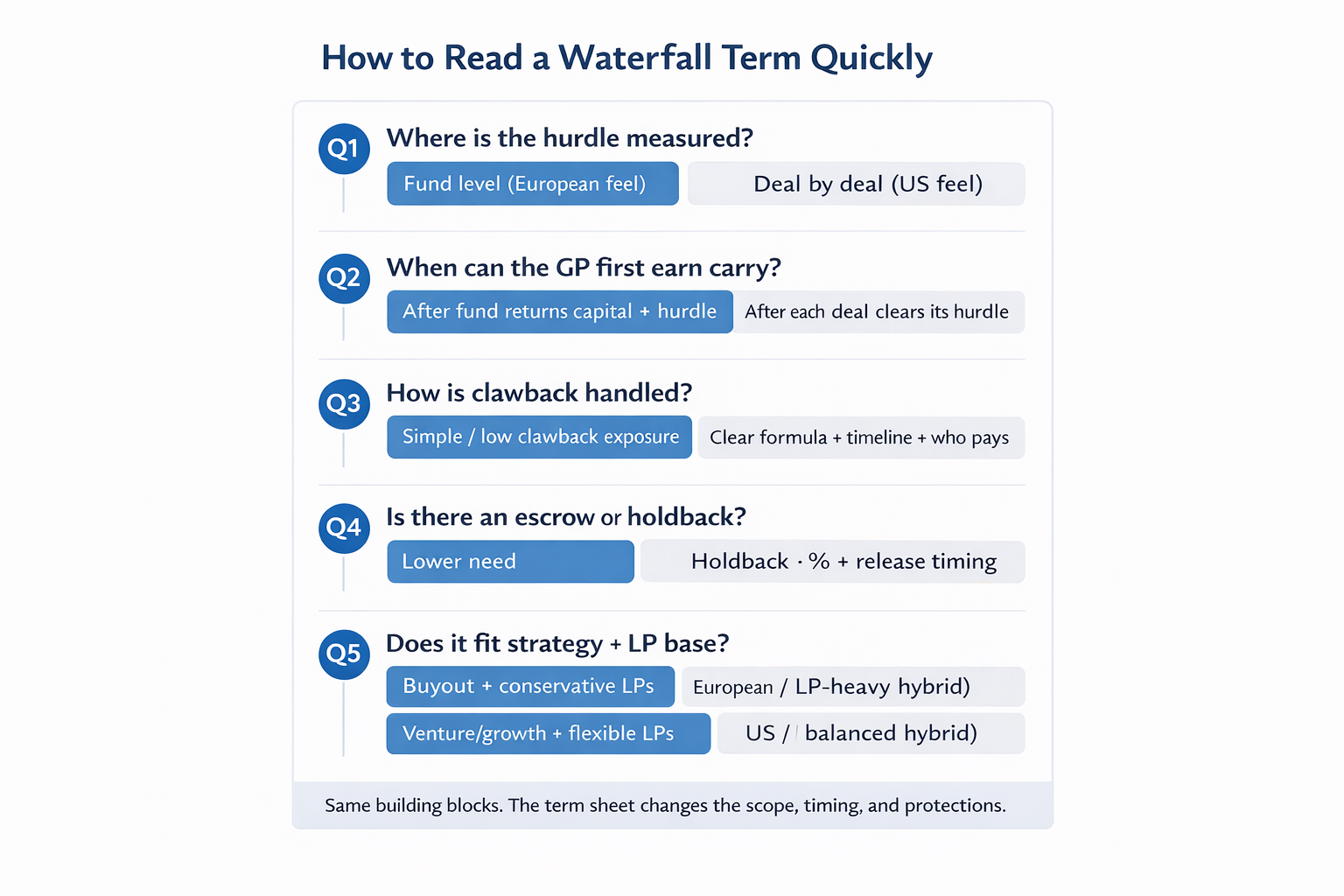

How to read a waterfall term quickly

When you see waterfall clauses in a limited partnership agreement or term sheet, you can decode them with a short checklist. After that, you can dive into the details.

Once you answer those questions, the labels become easy to translate.

- European waterfall: “Fund first, carry later, lower clawback risk.”

- US waterfall: “Deal first, carry sooner, requires strong clawback and controls.”

It needs to match the fund’s risk profile, the GP’s maturity and how much timing and complexity LPs are willing to take on for the specific manager in front of them.

_________________________

About Taghash

Taghash provides an end-to-end platform for venture funds, private equity, fund of funds, and other alternative investment funds. Over the last seven years, we have served as the tech arm for top VCs, helping them manage operations across deal flow, portfolio, fund, and LP management.

Trusted by leading fund managers like Blume Ventures, Kalaari Capital, and A91 Partners, we enable our clients to achieve greater success. Click here to book a demo.