Investment Fund Performance Metrics Explained for VC and PE Teams

Fund performance in VC and PE cannot be understood through a single metric. This blog explains how fund teams should assess performance through IRR, TVPI, DPI, RVPI, MOIC and benchmark context to build a more accurate view of value creation, realized returns and remaining portfolio exposure.

Measuring investment fund performance requires more than a single performance figure. In venture capital and private equity, performance needs to be assessed across multiple metrics, including capital called, cash distributed, unrealized portfolio value, valuation quality, fund maturity and benchmark relevance.

A fund may show strong paper value while returning limited cash to LPs. Another fund may show steady distributions even if its total multiple looks less aggressive. This is why GPs, LPs, fund finance teams and investment committees typically evaluate performance through a set of performance metrics.

In the current private markets environment, this has become even more important. Exit timelines, distribution pace and valuation quality are being reviewed more closely across fund reporting. LPs want to understand realized returns, liquidity and the quality of unrealized value.

Why Private Fund Performance Needs Multiple Metrics

Private funds operate differently from public market investments. LPs commit capital upfront, while the GP calls capital over time as investment opportunities arise. Portfolio companies mature over several years, exits happen at different points in the fund’s life and a meaningful portion of value may remain unrealized for long periods.

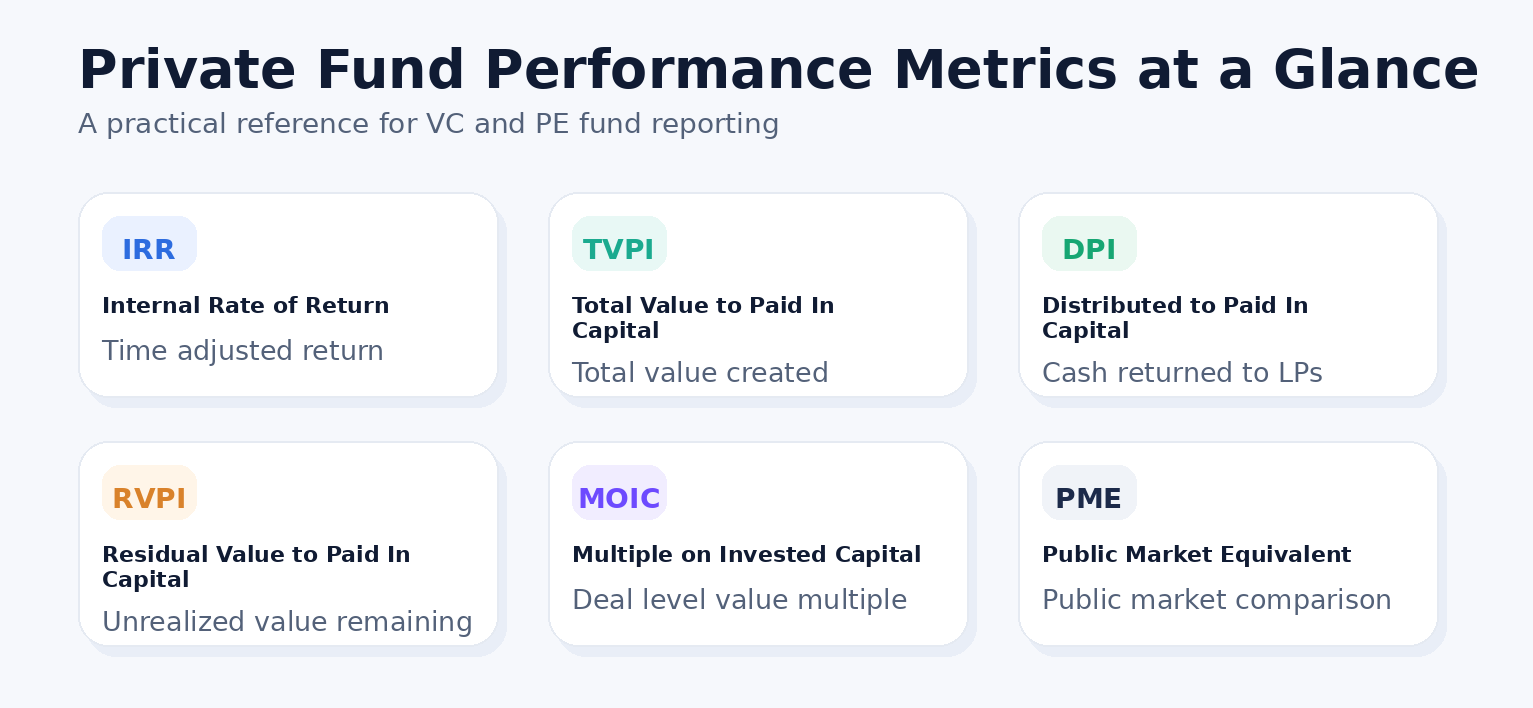

Because of this structure, a single metric cannot explain the complete performance picture. IRR shows time-adjusted performance. TVPI shows total value creation. DPI shows realized cash returned to LPs. RVPI shows value still held in the portfolio. MOIC helps assess deal-level value creation. PME compares private fund cash flows with a public market alternative.

These metrics help fund teams explain how value has been created, how much has been realized and how much remains dependent on future exits.

IRR Measures Time-Adjusted Return

Internal Rate of Return, or IRR, measures the annualized return of a fund based on the timing of capital contributions, distributions and residual value of unrealized holdings.

IRR is useful because private funds do not deploy and return capital in one movement. A fund that returns capital quickly can show a higher IRR than a fund that creates the same total value over a longer period. This makes IRR helpful when comparing funds with similar vintage, strategy, geography and cash flow patterns.

IRR needs careful interpretation. For active funds, IRR includes unrealized portfolio value. This means the number depends partly on valuation marks that may still need to be tested through exits. IRR should be reviewed alongside DPI, TVPI, RVPI and the fund’s valuation approach.

TVPI Measures Total Value Created

TVPI stands for Total Value to Paid In Capital.

TVPI = Distributions plus residual value divided by paid-in capital

A TVPI of 2.0x means the fund has created total value equal to two times the capital paid in by LPs. This includes cash already distributed and the remaining fair value of unrealized investments.

TVPI is especially useful in VC and growth equity because companies may stay private for many years before liquidity events occur. It is also useful in PE because it shows total value across exited and active portfolio companies.

An important consideration is valuation quality. Since TVPI includes unrealized value, it is only as reliable as the fund’s valuation process. Private capital teams should support unrealized value with a clear valuation methodology, documented assumptions and a consistent valuation review process.

DPI Measures Cash Returned to LPs

DPI stands for Distributed to Paid In Capital.

DPI = Distributions divided by paid-in capital

DPI shows how much cash has actually been returned to LPs. A DPI of 1.0x means LPs have received back an amount equal to their paid-in capital. A DPI above 1.0x means the fund has returned more cash than LPs have contributed.

DPI is one of the most important metrics for LPs because it reflects realized liquidity. In periods where exits are slower, LPs may review DPI more closely than paper value. A fund with high TVPI and low DPI may still depend heavily on future exits to convert unrealized value into cash.

DPI should always be interpreted with fund age and strategy. Early-stage VC funds often take longer to generate DPI because portfolio companies need time to mature. Mature PE or buyout funds are usually expected to show stronger distributions once they move deeper into the harvesting period.

Read more: Beyond DPI - How LPs Measure Private Equity Performance

RVPI Measures Remaining Unrealized Value

RVPI stands for Residual Value to Paid-In Capital.

RVPI = Residual value divided by paid-in capital

RVPI shows how much value remains inside the fund through active investments. A high RVPI may indicate a high-quality remaining portfolio with future value creation potential. It may also indicate that the fund is still dependent on future liquidity events.

For VC funds, RVPI is often higher during the early and middle years of the fund’s life because portfolio companies are still scaling. For PE funds, RVPI helps LPs understand how much value is still linked to future exits, refinancing, operational improvement or market conditions.

The quality of RVPI depends on portfolio concentration, company performance, valuation discipline and exit visibility.

MOIC Measures Deal Level Value Creation

MOIC stands for Multiple on Invested Capital.

MOIC = Total value divided by invested capital

MOIC is most useful at the investment or portfolio company level. A 3.0x MOIC means an investment is worth three times the capital invested.

In venture capital, MOIC helps identify power law return patterns, where a small number of companies may drive a large share of fund performance. In private equity, MOIC helps evaluate value creation from entry pricing, operating improvements, leverage reduction, add-on acquisitions and exit value.

At the fund level, TVPI or net multiple is usually the more appropriate performance measure because it connects directly to LP paid in capital, distributions and residual value.

Gross Returns and Net Returns

Gross returns show performance before management fees, fund expenses and carried interest. Net returns show what LPs receive after those costs.

Both serve different reporting purposes. Gross performance helps assess investment selection and portfolio management. Net performance reflects the LP outcome. For investor reporting, net performance usually carries greater relevance because it shows the actual return after fund economics.

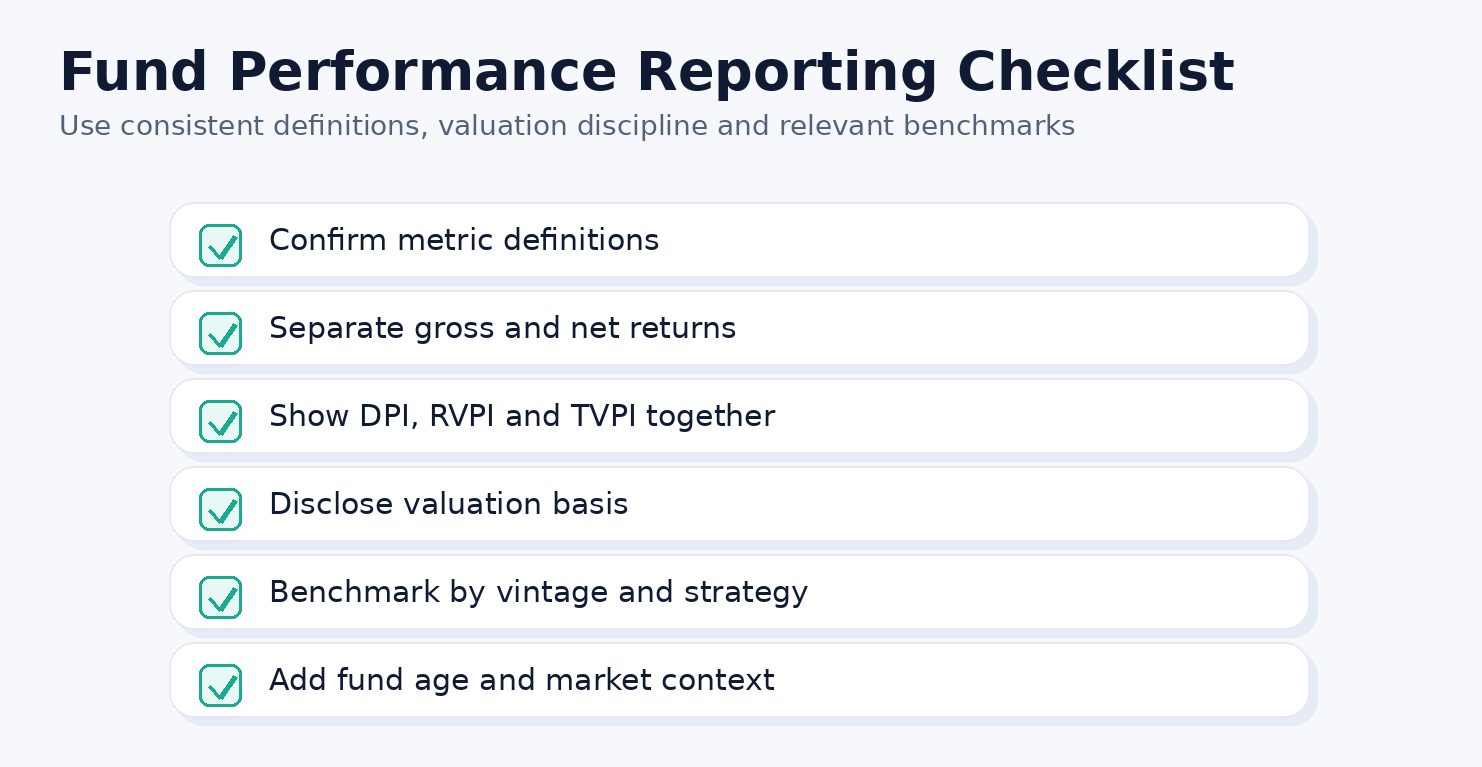

Private capital teams should clearly state whether performance metrics are gross or net, especially when reporting IRR, TVPI, DPI and multiples.

Benchmarking by Vintage, Strategy and Market Context

Benchmarking is essential because private fund performance is highly dependent on market cycle and vintage context. A VC fund should be compared with funds from a similar vintage, stage, geography and strategy. A PE or buyout fund should be compared with a relevant peer set, rather than a broad private capital universe.

The right benchmark should account for fund vintage, strategy, geography, stage or deal type, currency, fund size and gross or net basis.

Benchmark methodology also matters. Median, quartile, pooled, average and weighted benchmarks can produce different interpretations. A few larger funds or outlier exits can meaningfully influence benchmark data.

PME Compares Private Funds with Public Markets

Public Market Equivalent, or PME, compares private fund cash flows with a selected public market index using the same timing pattern.

PME helps LPs assess whether a private fund justified its illiquidity, risk and complexity compared with a public market alternative. For example, a growth equity fund may be compared with a relevant public equity index over the same contribution and distribution timeline.

PME is useful because private funds should be assessed against a public market alternative, along with peer group performance.

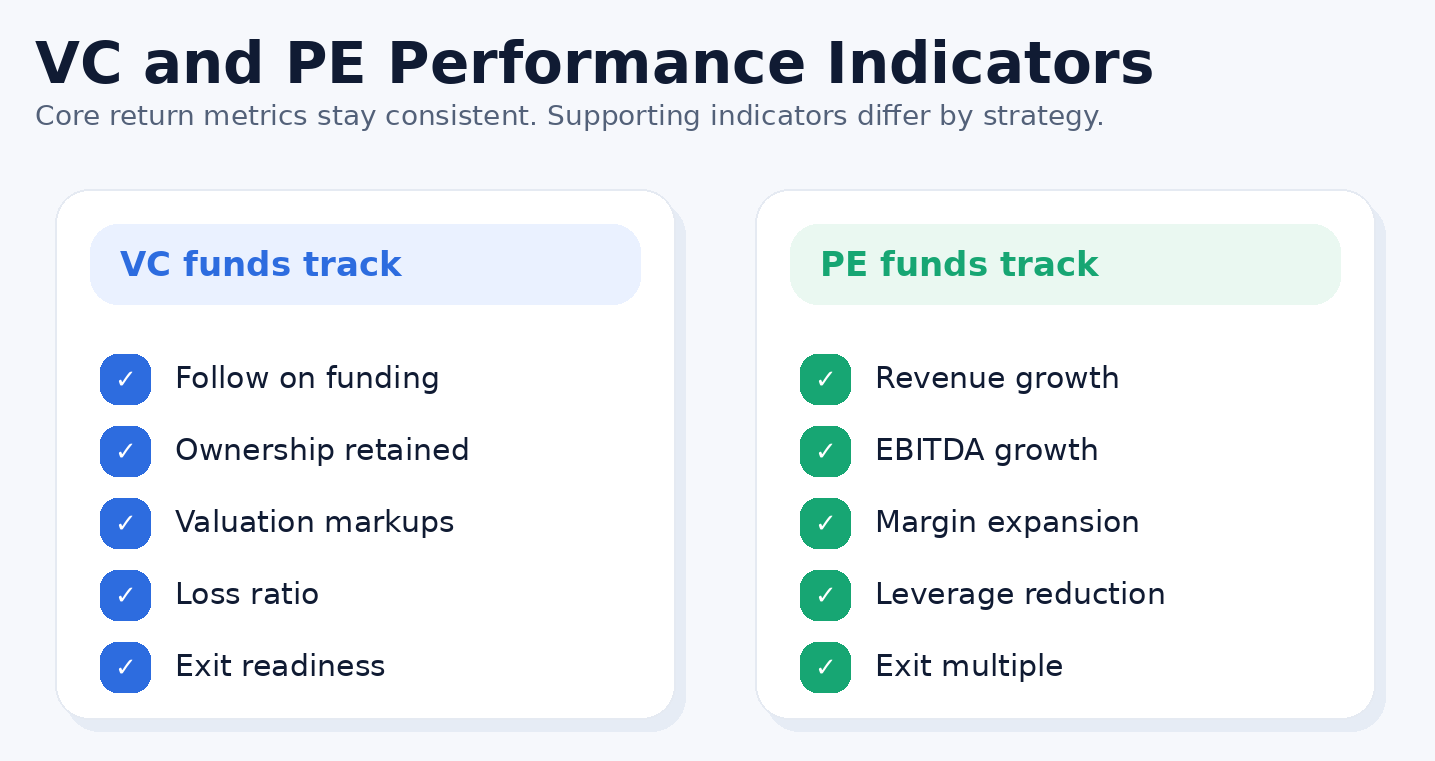

VC and PE Require Different Supporting Indicators

For VC funds, financial metrics should be read with portfolio quality indicators. These may include follow-on funding rates, graduation from seed to Series A or later rounds, ownership retained, valuation markups, loss ratio, concentration in top performers and exit readiness.

For PE funds, performance should also be assessed through operating indicators. These may include revenue growth, EBITDA growth, margin expansion, leverage reduction, cash conversion, add-on acquisition performance and exit multiple expansion.

These supporting indicators help explain the drivers and sustainability of returns.

Conclusion

Measuring VC and PE fund performance requires a connected view of multiple metrics. IRR shows time-adjusted return. TVPI shows the total value. DPI shows realized cash returned to LPs. RVPI shows the remaining unrealized value. MOIC explains deal-level value creation. PME compares fund outcomes with public market alternatives.

Credible private capital reporting should be clear, net of fees where relevant, supported by valuation discipline and benchmarked against the right vintage and strategy. LPs want to understand value creation, realized liquidity, residual exposure and performance quality against the right peer set.

About Taghash

Taghash provides an end-to-end platform for venture funds, private equity, fund of funds and other alternative investment funds. Over the last seven years, we have served as the tech arm for top VCs, helping them manage operations across deal flow, portfolio, fund and LP management.

We also offer a services layer to support execution across data management, legal and compliance, fund administration coordination, trustee and custodian interfacing and valuations and advisory.

Trusted by leading fund managers like Blume Ventures, Kalaari Capital and A91 Partners, we enable our clients to achieve greater success. Click here to book a demo.