Maturity Curve of a VC Firm

From friends-and-family Fund I to institution-backed Fund III, this blog breaks down how venture firms actually grow up in the eyes of LPs. It explores how reporting, governance and accredited investors shape that journey in the Indian context.

Every venture fund begins with conviction and relationships.

A few investors commit early because they believe in the person leading it as much as the investment thesis. These first LPs accept uncertainty and understand that the GP is starting a long journey that will test patience, judgment and discipline.

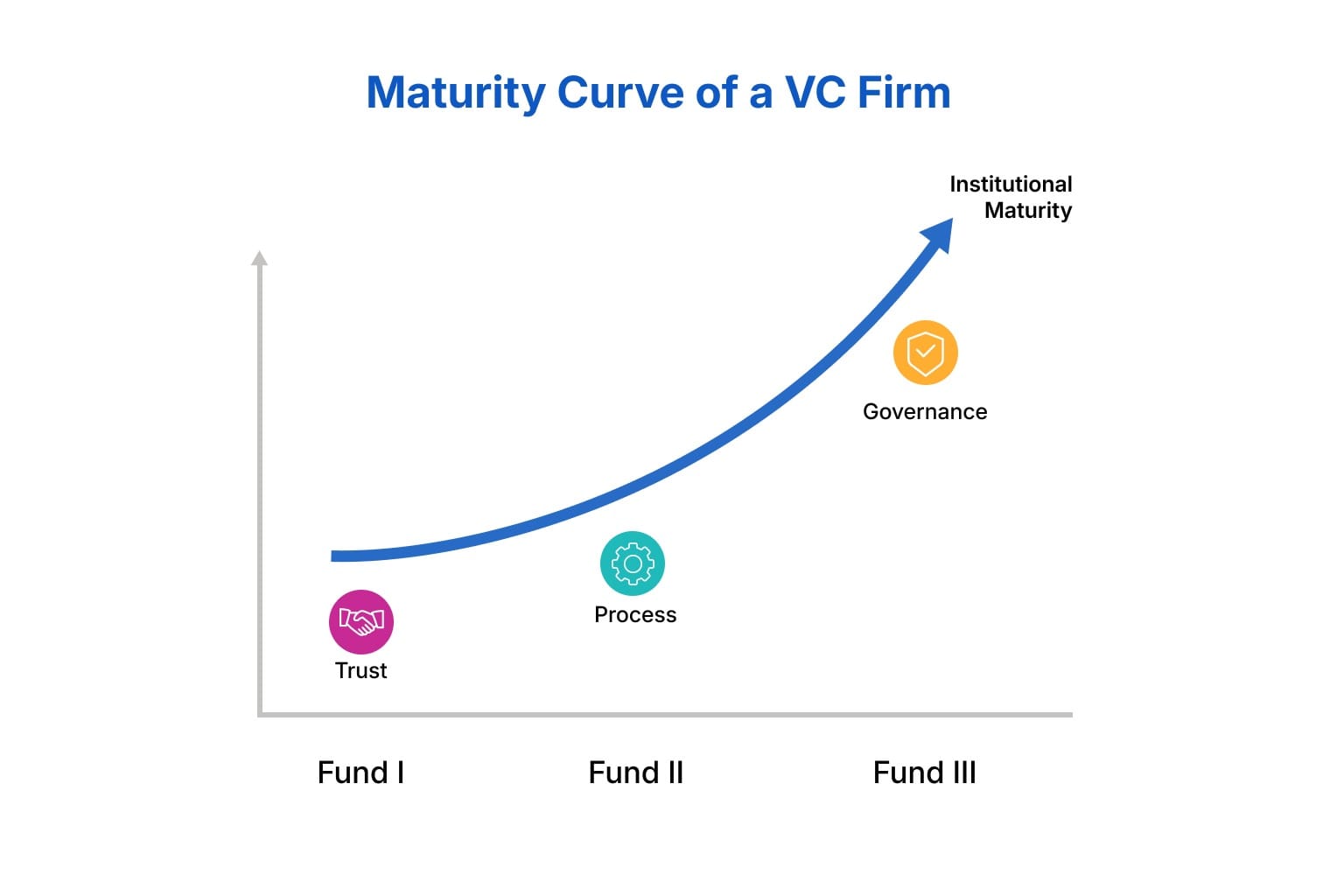

Fund I: Building Trust and Habits

Fund I is where credibility is first earned.

At this stage LPs are usually people who know or can vouch for the GP personally like former colleagues, mentors, founders or high-net-worth individuals. With little performance data available LPs value transparency and process discipline above all.

Timely reporting, documented decision-making and clear communication become early indicators of maturity. The size of the fund matters less than the consistency of behaviour. A GP who explains choices, stays accountable and operates with integrity through uncertainty begins to establish trust that lasts well beyond a single vintage.

Many LPs who stay through successive funds do so because they witnessed that discipline early. It becomes the foundation on which all later systems are built.

Fund II: Building Systems and Credibility

By Fund II, expectations rise.

The GP now carries a track record, a portfolio to report on and a small but meaningful history. LPs start evaluating both investment judgment and operational rigour. They observe how the GP manages audits, compliance, fund administration and governance.

Process and consistency begin to define quality. The rhythm of updates, accuracy of data and clarity of communication all shape LP confidence. The GP must demonstrate that Fund I’s results were the product of sound systems and improving decision frameworks.

Fund II is often the hardest phase to navigate. It requires moving from a founder-driven style to an institutional operating system without losing agility or culture. GPs who handle this transition with humility and structure earn lasting respect from early and new LPs alike.

Fund III: Running an Institution

By the third fund transformation becomes visible.

The LP base broadens to include institutions such as endowments, pensions, corporates and funds of funds. Scale increases and so do expectations. LPs now value process, performance and predictability in equal measure.

They expect the firm to operate independently of individuals and to deliver consistent clarity and control. Governance frameworks, ESG practices, risk reviews and independent audits become central to LP confidence.

At this stage the GP is expected to behave like a professional asset manager. Decision making is documented, reporting is rhythmic and communication is deliberate. Continuity across funds signals institutional maturity. The credibility of a firm lies in the steadiness of its systems and the quality of its relationships.

How the LP Mix Evolves

In early funds a majority of commitments usually come from individuals, family offices and close networks. Institutional participation is rare at this point. As the GP demonstrates proof of discipline and early exits institutions begin to engage.

By the second or third fund this mix changes significantly. Institutional LPs such as pensions, endowments and development funds start to dominate the capital base providing stability and larger ticket sizes.

LPs reward composure and stability more than expansion for its own sake.

While global studies suggest that 50–80% of Fund I commitments often come from private investors, proportions vary by geography and strategy. In India institutional LP participation in early-stage venture capital remains limited so GPs rely heavily on founder networks and family offices before larger institutions enter.

The Role of Accreditation in India

India’s regulatory framework for Accredited Investors (AIs) introduced by SEBI has begun to support this path to maturity.

To qualify investors must meet prescribed income or net worth thresholds such as a net worth of ₹7.5 crore or annual income above ₹2 crore with part of assets held in financial form. SEBI has authorised agencies such as CDSL Ventures Limited (CVL) and NSDL’s NDML to issue accreditation certificates valid for multiple years.

There is also active discussion around introducing AI-only AIF schemes with lighter regulatory requirements. For first-time managers having accredited investors in the initial LP base provides a compliance signal. It shows that the fund operates within recognised financial and disclosure standards which builds comfort for future institutional investors.

Body corporates excluding family trusts generally face higher thresholds often around ₹50 crore in net worth to qualify for accreditation. This framework brings greater clarity to the investor ecosystem and gradually institutionalises early-stage capital.

The Path of Maturity

As funds progress from Fund I to Fund III expectations shift decisively:

- Fund I: LPs assess integrity, judgment and discipline

- Fund II: LPs look for consistency, systems and process

- Fund III: LPs expect governance, predictability and institutional control

A venture firm matures when instinct evolves into repeatable systems and improvisation gives way to structure. Each stage tests a different skill such as staying consistent under stress, scaling process without loss of agility and leading responsibly.

Firms that grow through these phases build credibility by evolving with steadiness. Their maturity lies in systems that outlast individuals and relationships that deepen with time.