Side Letters Post Pari Passu: What Still Survives (and What Doesn’t)

Pari passu is now the baseline for AIF investor rights under Regulation 20(22), so side letters must fit within a disclosed framework. This blog explains what still survives under the SFA positive list and SEBI principles, plus a practical drafting checklist for fund managers.

Side letters have always been part of India’s AIF fund formation toolkit. They helped managers close anchor investors, navigate institutional policy constraints and tailor reporting or fee mechanics without rewriting the entire fund document set.

That flexibility is now materially constrained. SEBI has hard-coded a pari passu baseline for AIF investor rights and pushed the market toward standardised, disclosed and eligibility-based differential rights. In practice, this changes what you can put in a side letter and how you have to operationalise it.

The regulatory pivot

Pari passu is now the default rule, not a drafting preference

Regulation 20(22) (inserted via the Fifth Amendment in November 2024) requires that investor rights in a scheme, other than pro rata rights, must be pari passu “in all aspects”. Differential rights are permitted only if offered in the manner specified by SEBI and only if they do not affect the interests of other investors. There is a specific exemption for Large Value Funds for Accredited Investors (LVFs).

SEBI’s “how” is as important as the “what”

SEBI’s December 13, 2024, circular sets guiding principles that function like a gating test for any differential right. It also requires that differential rights be provided only in accordance with the SFA’s implementation standards and be transparently disclosed, including eligibility and opt-in availability for any investor meeting the eligibility criteria.

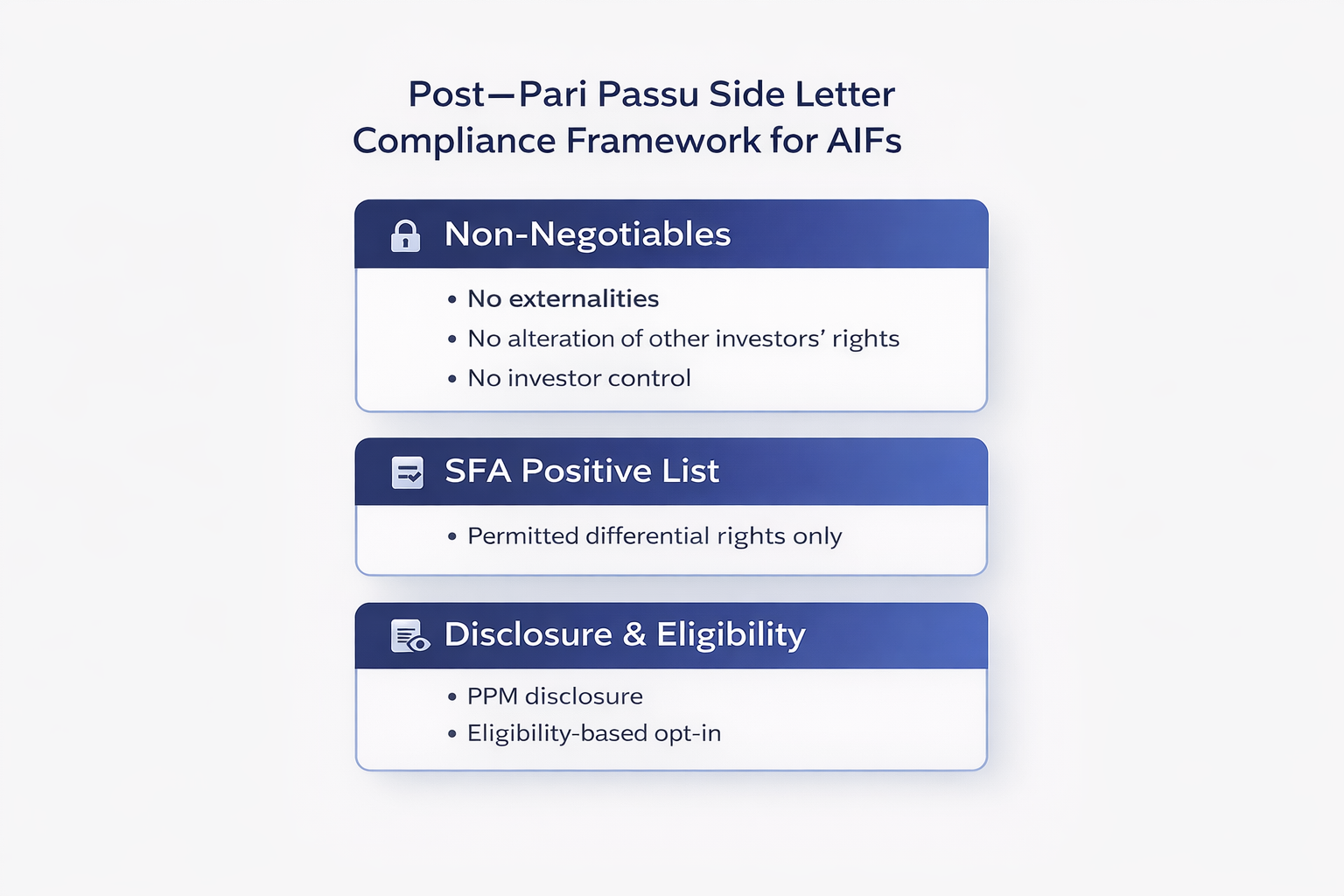

The new compliance architecture for side letters

Think of the post-pari passu regime as a three-layer filter.

Layer 1. The non-negotiables

A side letter cannot.

- Shift a cost, liability, or economic burden of one investor onto other investors.

- Alter rights available to other investors under their agreements.

- Grant “control” through non-monetary rights, except where the investor nominee sits on a committee constituted under Regulation 20(7).

Layer 2. The “positive list” of permissible differential rights

The SFA implementation standards specify a positive list of ten categories where differential rights may be offered, subject to conditions. These are the main buckets within which side letters still survive.

Layer 3. Disclosure plus eligibility discipline

Even if a right is within the positive list, the PPM must.

- State the eligibility criteria for each differential right.

- Provide that any investor meeting the criteria may opt to avail it.

This is the structural end of “secret side letters” in any meaningful sense. The market can still negotiate. The negotiation must fit inside a disclosed and extendable framework.

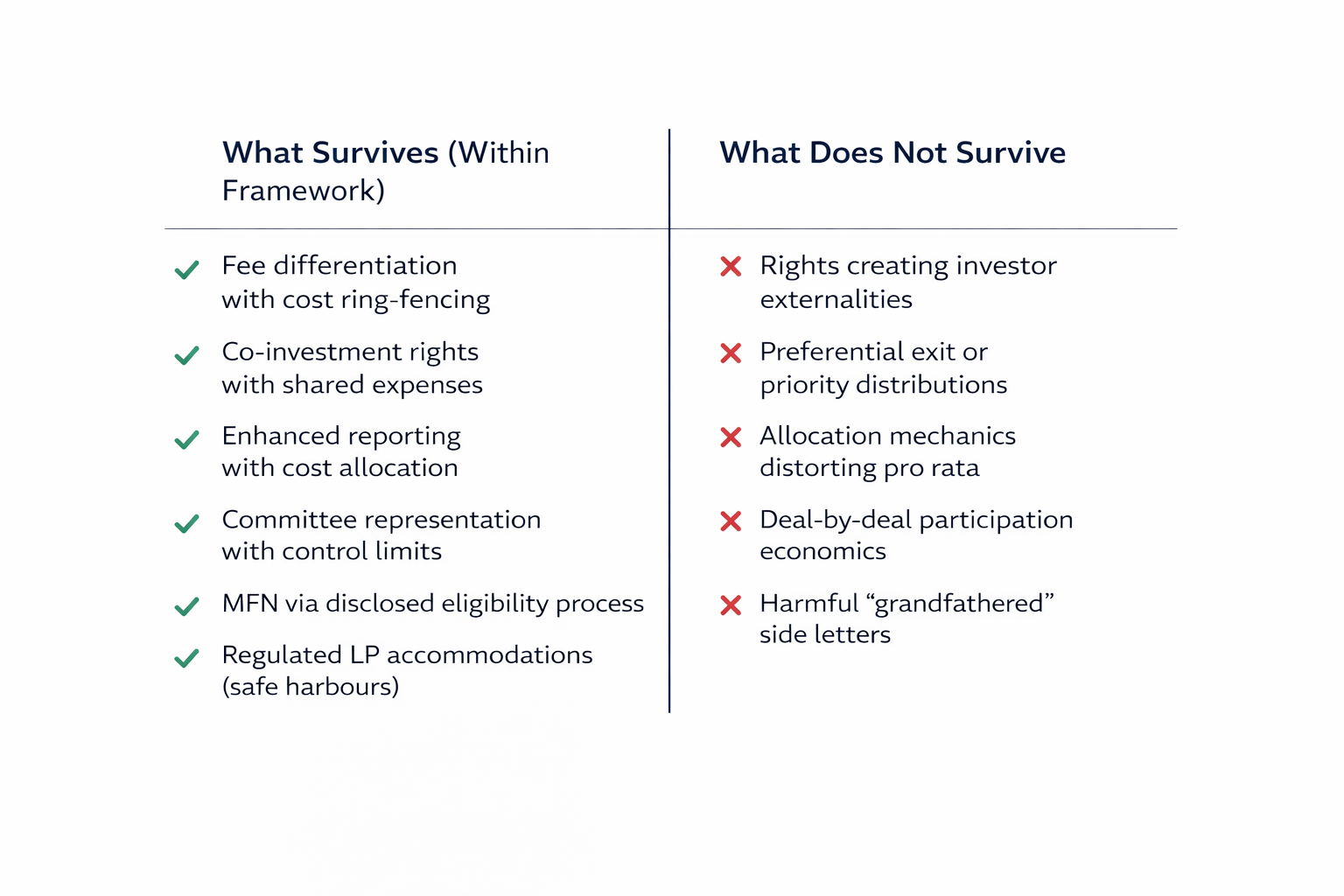

What still survives in side letters

Below is what continues to be viable, typically via side letters, separate unit classes, or a structured election process, but only if you stay within the SFA list and the SEBI guiding principles.

1. Fee and expense differentiation, with strict cost allocation

Permitted categories include.

- Fund expenses. Waiver or reduction is permitted, but any incremental expense pushed onto others must instead be borne by the manager or sponsor, not the fund and not other investors.

- Management fee.

- Hurdle rate of return.

- Carried interest calculations.

Practical drafting note. Expense-related side letters need careful “no externality” language plus an internal accounting mechanism. If the fund’s administrator cannot ring-fence the cost, it becomes non-compliant in effect even if compliant in form.

2. Co-investment rights, with proportional expense sharing

Co-investment rights remain permissible. The condition is that common expenses relating to the co-investment must be shared proportionately between the AIF and co-investors.

3. Enhanced reporting and information rights, with two carve-outs

Additional information or higher frequency reporting can be given to select investors, but it cannot include.

- Anything that would breach applicable law.

- Any information that should be provided or available to all investors.

Costs of providing such additional reporting must be charged only to the relevant investors or to the manager or sponsor, not to the fund or other investors.

This is a major survival zone for institutional LP side letters, but it now requires a clear line between “enhanced” reporting and “withheld” reporting.

4. Committee representation, with control constraints

Select investors may nominate a member on committees of the AIF or scheme, subject to AIF Regulations and specified conditions (term, tenure, voting, information, etc.).

Key compliance point is that this cannot become de facto negative control over investment decisions unless the structure is within Regulation 20(7) committee constructs and does not amount to investor control of the scheme.

5. MFN survives, but it is now explicitly within the framework

Most Favoured Nation is explicitly permitted as a differential right category.

What changes is operational. MFN needs to be administered as a disclosed election process, anchored to eligibility criteria, not as a bilateral, opaque promise.

6. Confidentiality of investor information, but only with explicit consent

Sharing details of other investors with select investors is allowed only with the specific and explicit consent of the investor whose information is being shared.

7. Representations and warranties, but they cannot create extra rights

Representations and warranties can be provided to select investors, but they must not result in any “right” being provided to such investors.

In practice, this pushes managers to treat such provisions as confirmations and undertakings, not as triggers for bespoke remedies that other investors do not have.

8. Two important “not a differential right” safe harbours

Two items are expressly not treated as differential rights.

- Information that merely elaborates fund documents in line with AIF Regulations and circulars.

- Specific treatment is needed for an investor to comply with laws or regulations applicable to it.

This is a crucial drafting route for regulated LPs. For example, AML, sanctions, public procurement, or internal policy-driven covenants may fit here, provided they do not create externalities for other investors.

What does not survive, or survives only in a narrow, regulated form

1. Any right that creates investor externalities

If a side letter results in other investors bearing a liability or cost that properly belongs to the favoured investor, it fails the SEBI guiding principle.

Historically common examples include.

- Indemnity caps or liability caps that effectively push uncovered liabilities to the rest of the LP base.

- Waivers of equalisation or warehousing costs that are then absorbed by the fund pool.

- Late-close “at cost” mechanics where the value leakage is borne by existing LPs.

These are precisely the kinds of outcomes SEBI flagged as problematic in its board material leading up to the amendments.

2. Preferential exit and “priority distribution” for non-exempt investors

AIF structures that used senior and junior classes to create priority distribution waterfalls have been under SEBI restriction. Post the pro rata regime, existing schemes using priority distribution models that do not fall within specified exemptions cannot accept fresh commitments or make new investments.

3. Drawdown and allocation side letters that distort pro rata

Even where the issue is framed as “commercial convenience”, pro rata rights under Regulation 20(21) mean that investors must have rights pro rata to their commitment in each investment and in distributions, subject to specified exceptions (excuse, exclusion, default and carry sharing).

SEBI’s November 2025 draft circular shows the direction of travel. It proposes to formalise how drawdowns can be done based on commitment or undrawn commitment, requires upfront disclosure and restricts mid-tenure changes. It also proposes guardrails to prevent drawdown methodologies from causing disproportionate stakes in investee companies relative to concentration limits.

This materially narrows bespoke side letter mechanics that change participation economics deal by deal, outside of excuse or exclusion logic.

4. “Grandfathered forever” is not available for harmful differential rights

For existing schemes whose PPMs were filed on or after March 1, 2020, managers had to report differential rights not covered by the SFA standards and immediately terminate or discontinue those that affect other investors’ rights.

So legacy side letters can survive only if they pass the new tests. Otherwise, they become a compliance remediation exercise.

The LVF carve-out: Where side letters can still be more bespoke

LVFs can avail an exemption from the pari passu requirement, subject to disclosure in the PPM and obtaining an investor undertaking acknowledging that differential rights may be offered, which might affect the interests of other investors. Existing LVFs can also avail this exemption with specific investor waivers.

This is not a free pass for anything. It is a structured waiver regime. Managers should treat it as higher litigation and relationship risk, even if technically permissible.

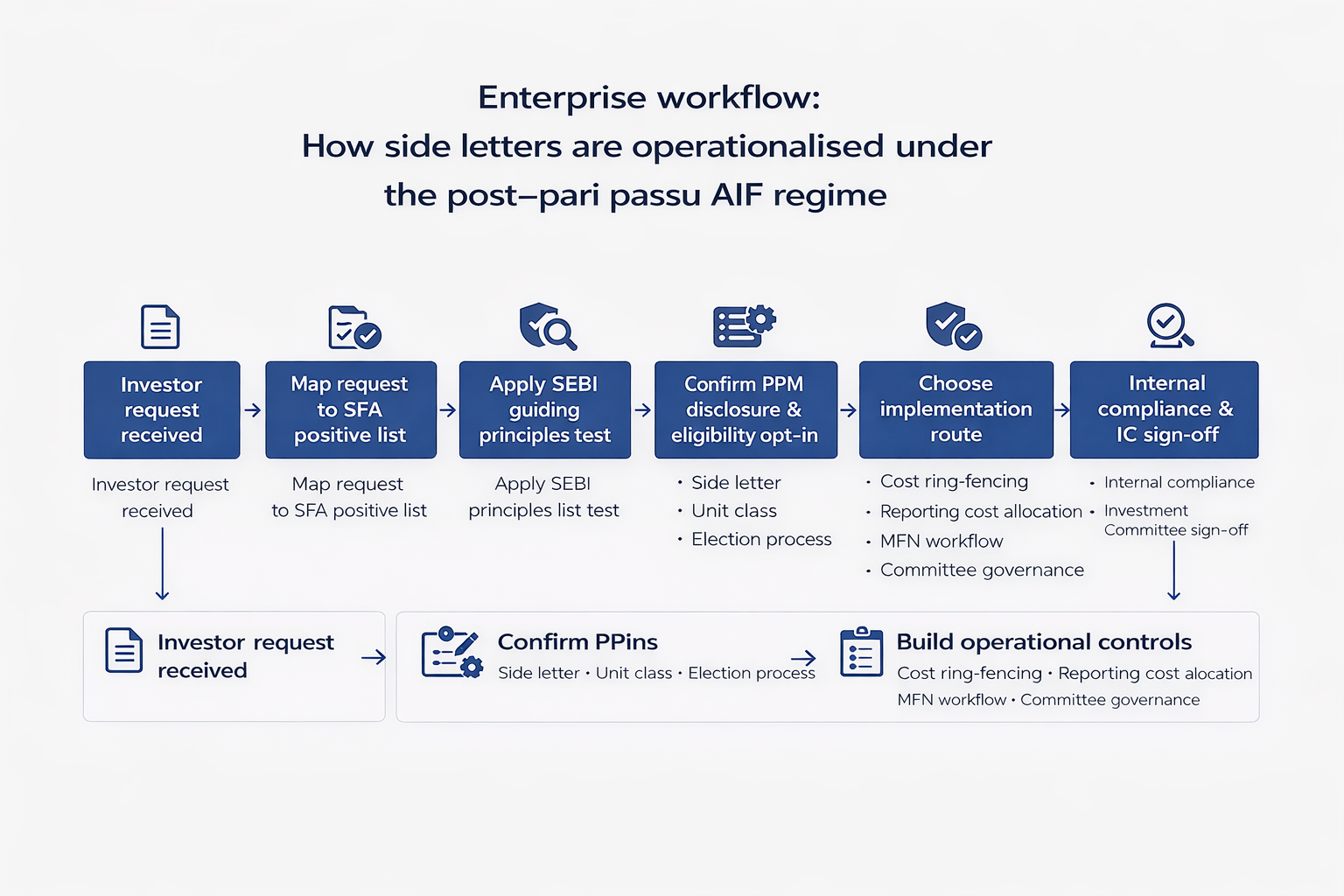

A practical drafting checklist for side letters post-pari passu

- Map the ask to the SFA positive list bucket. If it does not fit, treat it as high risk and assume it will need restructuring.

- Run the SEBI guiding principles test. No externality, no alteration of others’ rights, no control through non-monetary rights.

- Ensure PPM disclosure and eligibility-based opt-in. Drafting a side letter that only one investor can ever qualify for is now structurally fragile.

- Build an operational mechanism. Cost ring-fencing, reporting cost allocation, MFN election workflow and committee governance processes. The compliance breach will often be operational, not textual.

- For regulated LP accommodations, use the “not a differential right” safe harbours carefully. Document the regulatory rationale and confirm no adverse impact on other investors.

The bottom line

Side letters are not dead. Bilateral, opaque, preference-creating side letters are.

What survives is a narrower, standardised category of differential rights that can be justified as non-prejudicial to other investors, disclosed in the PPM and offered through a transparent eligibility framework. What does not survive is anything that changes the economic or liability position of the investor pool in a way that makes some investors subsidise others.